Mortgage Interest Rates Explained

Mortgage interest rates affect how much it costs to borrow money to buy a home. A small difference in rate can change your monthly payment, the total interest you pay over the life of the loan, and even the price range you can realistically afford.

This matters whether you are buying your first home, refinancing an existing mortgage, comparing loan offers, deciding between a fixed-rate and adjustable-rate mortgage, or wondering whether paying discount points makes sense. Many borrowers focus on the home price, but the interest rate, fees, loan term, and loan structure can be just as important to long-term affordability.

The main concern for most readers is simple: how do I know whether a mortgage rate is fair, and what can I do to improve it? This guide explains mortgage interest rates in plain English, shows how lenders price loans, compares common rate options, and gives practical steps you can take before you apply.

1. What Is a Mortgage Interest Rate?

A mortgage interest rate is the percentage a lender charges you each year to borrow money for a home loan. It is applied to the unpaid loan balance, not the original home price. Your monthly mortgage payment usually includes principal and interest, and may also include property taxes, homeowners insurance, mortgage insurance, and escrow payments.

Concise definition: A mortgage interest rate is the cost of borrowing money to buy or refinance a home, expressed as an annual percentage of your remaining loan balance.

| Term | Plain-English Meaning | Why It Matters |

|---|---|---|

| Interest rate | The annual cost of borrowing, expressed as a percentage. | Drives the principal-and-interest portion of your payment. |

| APR | Annual percentage rate, which includes interest plus certain loan costs. | Helps compare the total cost of different loan offers. |

| Principal | The amount you borrowed and still owe. | Interest is charged on this balance. |

| Loan term | How long you have to repay the mortgage. | Affects payment size and total interest paid. |

| Rate lock | A lender agreement to hold a quoted rate for a set period. | Protects you if rates rise before closing. |

| Discount points | Upfront fees paid to lower the rate. | May save money if you keep the loan long enough. |

2. How Mortgage Interest Rates Work

Mortgage interest is usually amortized, which means each payment is split between interest and principal. Early in the loan, more of the payment goes toward interest because the loan balance is still high. Over time, as the balance falls, more of each payment goes toward principal.

- You borrow a principal amount from a lender.

- The lender charges interest on the outstanding balance.

- Your monthly payment is calculated based on the loan amount, interest rate, and loan term.

- Each payment first covers interest due for that month; the rest reduces principal.

- As principal declines, the interest portion falls and the principal portion rises.

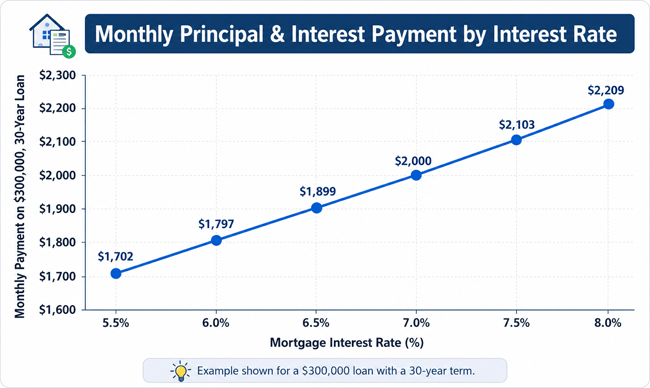

2.1 Example: How a Rate Change Affects Payment

Assume a $300,000 fixed-rate mortgage with a 30-year term. The examples below show principal and interest only. They do not include taxes, insurance, HOA dues, mortgage insurance, or closing costs.

| Interest Rate | Estimated Monthly Principal & Interest | Estimated Interest Over 30 Years |

|---|---|---|

| 5.5% | $1,703 | $313,212 |

| 6.0% | $1,799 | $347,515 |

| 6.5% | $1,896 | $382,633 |

| 7.0% | $1,996 | $418,527 |

| 7.5% | $2,098 | $455,152 |

| 8.0% | $2,201 | $492,466 |

Chart: Example payment impact for a $300,000, 30-year fixed mortgage. Actual payments vary by loan terms and lender fees.

3. Why Mortgage Interest Rates Matter

- Affordability: A higher rate can reduce how much house you can comfortably afford.

- Monthly cash flow: Your rate affects the payment you must make every month.

- Total lifetime cost: A higher rate can add tens or hundreds of thousands of dollars of interest over a long loan term.

- Refinancing decisions: Current rates influence whether refinancing could save money.

- Home-buying strategy: Rate changes may affect timing, budget, and whether to buy down the rate.

4. Interest Rate vs APR: What Is the Difference?

The interest rate tells you the cost of borrowing before many fees. APR, or annual percentage rate, is broader because it includes the interest rate plus certain lender charges and prepaid costs. The Consumer Financial Protection Bureau emphasizes that interest rate is important, but fees, points, mortgage insurance, and closing costs also affect the total cost of a mortgage.

| Comparison | Interest Rate | APR |

|---|---|---|

| What it measures | Cost of borrowing the principal. | Estimated annualized cost including interest and certain fees. |

| Best for | Estimating monthly principal-and-interest payment. | Comparing overall loan cost between lenders. |

| Includes lender fees? | Usually no. | Often yes, depending on the fee type. |

| Can it be lower than APR? | Usually yes. | Usually equal to or higher than the interest rate. |

| Common mistake | Choosing the lowest rate while ignoring high fees. | Assuming APR is perfect for every scenario, even when selling or refinancing soon. |

5. What Affects Mortgage Interest Rates?

Mortgage rates are shaped by two broad categories: market conditions and borrower-specific risk. You cannot control the bond market, inflation, or lender funding costs. You can influence many personal factors, such as credit, down payment, debt level, loan type, and comparison shopping.

5.1 Market Factors Borrowers Cannot Control

- Inflation expectations: Higher inflation often pushes long-term interest rates higher.

- Treasury yields: The 10-year Treasury yield is a common benchmark for 30-year mortgage pricing, though mortgage rates also include additional spreads and lender costs.

- Mortgage-backed securities: Investors price mortgage loans in secondary markets, affecting rates offered to consumers.

- Economic growth and employment: Strong growth can push rates up; economic uncertainty can move rates in either direction depending on investor behavior.

- Federal Reserve policy: The Fed does not directly set mortgage rates, but its policy decisions influence credit markets and rate expectations.

5.2 Personal Factors Borrowers Can Influence

| Factor | How It Can Affect Your Rate | What You Can Do |

|---|---|---|

| Credit score | Stronger credit may qualify for better pricing. | Pay on time, reduce credit card balances, correct report errors. |

| Down payment / loan-to-value | More equity can reduce lender risk. | Save more, compare low-down-payment programs carefully. |

| Debt-to-income ratio | High monthly debts can make approval riskier. | Pay down debts or choose a more affordable price range. |

| Loan type | Conventional, FHA, VA, USDA, jumbo, and non-QM loans price differently. | Compare programs, not just lenders. |

| Loan term | 15-year loans often have lower rates but higher payments than 30-year loans. | Choose a term that fits both cash flow and long-term goals. |

| Property type and occupancy | Investment properties and second homes may cost more to finance. | Be honest about occupancy and compare eligible products. |

| Points and credits | Paying points may lower the rate; lender credits may raise it. | Calculate break-even time before choosing. |

6. Types of Mortgage Interest Rates

6.1 Fixed-Rate Mortgage

A fixed-rate mortgage has an interest rate that stays the same for the life of the loan. The principal-and-interest payment does not change, although taxes, insurance, HOA dues, and escrow payments can still rise. Fixed rates are popular with borrowers who value stability and plan to keep the home for a long time.

6.2 Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage has an interest rate that can change after an initial fixed period. For example, a 5/6 ARM may have a fixed rate for five years and then adjust every six months. ARMs usually include adjustment rules, index, margin, and caps that limit how much the rate can change.

| Feature | Fixed-Rate Mortgage | Adjustable-Rate Mortgage |

|---|---|---|

| Payment predictability | High. Principal and interest stay stable. | Lower after the fixed period because the rate can adjust. |

| Starting rate | Often higher than an ARM introductory rate. | May start lower, depending on market conditions. |

| Best fit | Long-term owners and risk-averse borrowers. | Borrowers who may sell, refinance, or pay off the loan before adjustments. |

| Main risk | You may pay more if market rates later fall and you do not refinance. | Payment shock if the rate rises after the introductory period. |

| Key documents to review | Loan Estimate and Closing Disclosure. | Loan Estimate, ARM program disclosure, caps, index, and margin. |

7. Mortgage Points, Lender Credits, and Rate Buydowns

7.1 Discount Points

Discount points are upfront fees paid to the lender in exchange for a lower interest rate. One point typically equals 1% of the loan amount, but one point does not always reduce the rate by the same amount. The value depends on the lender, market, loan type, and timing.

The key question is break-even: how long will it take for monthly savings to exceed the upfront cost?

| Scenario | Example |

|---|---|

| Loan amount | $300,000 |

| Cost of 1 point | $3,000 |

| Monthly savings from lower rate | $75 |

| Break-even period | $3,000 / $75 = 40 months |

Practical takeaway

If you expect to keep the loan longer than about 40 months, paying the point may help. If you expect to sell or refinance sooner, it may not.

7.2 Lender Credits

A lender credit works in the opposite direction. You accept a higher interest rate in exchange for the lender covering some closing costs. This can help if cash is tight at closing, but it may cost more over time if you keep the mortgage for many years.

7.3 Temporary Rate Buydowns

A temporary buydown reduces the payment for a short period, such as the first one or two years. It can make early payments easier, but borrowers should qualify based on the long-term payment they will owe after the buydown ends.

8. Step-by-Step Process: How to Compare Mortgage Interest Rates

- Check your credit reports and fix errors before applying.

- Establish a realistic home-buying budget using the full payment, not just principal and interest.

- Get quotes from multiple lenders on the same day because rates change frequently.

- Ask each lender for the same loan type, loan term, down payment, rate-lock period, and points structure.

- Compare the Loan Estimate, especially the interest rate, APR, origination charges, points, lender credits, mortgage insurance, and cash to close.

- Calculate the monthly payment difference and the total cost over your expected time in the home.

- Decide whether to lock the rate based on your closing timeline and risk tolerance.

- Keep your credit and finances stable until closing; avoid new debt, missed payments, or large unexplained deposits.

9. Costs and Fees Related to Mortgage Rates

A low advertised rate does not always mean the cheapest mortgage. Rates are often connected to fees, points, and credits. Always compare written Loan Estimates, not verbal quotes.

| Cost or Fee | What It Means | How It Relates to Rate |

|---|---|---|

| Origination charge | Lender fee for making the loan. | A lower rate may come with higher origination costs. |

| Discount points | Upfront prepaid interest. | Can lower the rate if the borrower pays more at closing. |

| Lender credit | Credit toward closing costs. | Usually comes with a higher rate. |

| Mortgage insurance | Insurance required on some low-down-payment loans. | Does not change the note rate but increases total monthly cost. |

| Rate-lock fee or extension | Cost to hold or extend a quoted rate. | May apply if closing takes longer than expected. |

| Third-party fees | Appraisal, title, recording, credit report, and settlement fees. | Usually affect cash to close more than the rate. |

10. Benefits of Understanding Mortgage Interest Rates

- You can compare offers more confidently.

- You can avoid being distracted by a low rate paired with high fees.

- You can choose between fixed and adjustable rates based on your real plans.

- You can decide whether paying points, accepting credits, or refinancing makes sense.

- You can protect your budget from payment shock and long-term interest costs.

11. Risks and Trade-Offs to Understand

| Risk | Why It Matters | How to Reduce It |

|---|---|---|

| Rate shopping without matching terms | Quotes are not comparable if points, term, lock period, or loan type differ. | Ask for same-day Loan Estimates with identical assumptions. |

| Payment shock on ARMs | Payment may rise after the introductory period. | Understand caps, index, margin, and worst-case payment. |

| Paying points without staying long enough | Upfront cost may not be recovered. | Calculate break-even and consider your likely move/refinance timeline. |

| Ignoring APR and fees | Lowest rate may hide higher total costs. | Compare APR, lender fees, and cash to close. |

| Assuming the Fed directly sets mortgage rates | Mortgage rates can move even when Fed policy does not change. | Watch broader market rates and get updated lender quotes. |

| Overborrowing because the lender approves you | Approval does not guarantee comfort. | Build a personal budget with taxes, insurance, maintenance, and emergency savings. |

12. Real-World Mortgage Rate Examples

12.1 Example 1: The First-Time Buyer Comparing Two Lenders

Maya is buying a $350,000 home with 10% down. Lender A offers a lower interest rate but charges more in points. Lender B offers a slightly higher rate with lower closing costs. Maya plans to move within four years. After calculating the break-even point, she realizes Lender B may be better because she may not keep the loan long enough to recover the upfront cost of points.

12.2 Example 2: The Homeowner Considering a Refinance

Daniel already has a mortgage. A lender offers a refinance with a lower rate, but the closing costs are significant. Daniel divides the closing costs by the monthly savings to estimate the break-even period. If he expects to sell before break-even, refinancing may not be worth it even though the rate is lower.

12.3 Example 3: The Borrower Choosing Fixed vs ARM

Sara expects to relocate for work within five years. A fixed-rate mortgage offers stability, but an ARM has a lower introductory payment. Sara compares the worst-case ARM adjustment and decides whether the lower short-term cost is worth the future uncertainty.

13. Expert Tips to Get a Better Mortgage Rate

- Improve your credit before applying. Even small credit improvements can affect pricing tiers.

- Compare at least three lenders, including a bank, credit union, mortgage broker, or online lender.

- Ask whether the quote includes points. A rate without fee context is incomplete.

- Use the Loan Estimate, not marketing language, to compare offers.

- Choose the right loan term. A 15-year mortgage may have a lower rate but a much higher payment.

- Do not drain emergency savings just to make a larger down payment or pay points.

- Lock your rate when the payment works for your budget and your closing timeline is realistic.

- Avoid major financial changes before closing, such as opening new credit cards or financing furniture.

14. Common Mistakes to Avoid

| Mistake | Why It Hurts | Better Approach |

|---|---|---|

| Shopping by interest rate only | Fees can make a low-rate offer more expensive. | Compare APR, points, cash to close, and total cost. |

| Not comparing multiple lenders | One lender may not offer your best available pricing. | Get several written quotes on the same day. |

| Ignoring the rate lock | Rates can change before closing. | Understand lock length, cost, and extension rules. |

| Assuming advertised rates apply to everyone | Ads may assume excellent credit, large down payment, or points. | Ask for a quote based on your actual profile. |

| Choosing an ARM without understanding caps | Future payments may rise substantially. | Review index, margin, adjustment frequency, and caps. |

| Paying points automatically | Points only help if the savings exceed upfront cost. | Calculate break-even and consider how long you will keep the loan. |

| Borrowing up to the approval limit | Lender approval may exceed your comfort zone. | Set your own budget with maintenance and savings included. |

15. Quick Action Checklist

- Check your credit reports before applying.

- Estimate your full monthly housing cost, including taxes and insurance.

- Decide how long you realistically expect to keep the home or loan.

- Get at least three same-day mortgage quotes.

- Ask whether each quote includes discount points or lender credits.

- Compare Loan Estimates line by line.

- Calculate break-even before paying points or refinancing.

- Review ARM caps and worst-case payments if considering an adjustable rate.

- Lock the rate once you are comfortable with the offer and timeline.

- Keep finances stable until the mortgage closes.

16. Pros and Cons of Focusing on a Lower Mortgage Rate

| Pros | Cons |

|---|---|

| Can lower monthly payment. | May require higher upfront points or fees. |

| Can reduce total interest over time. | Lowest rate may not be best if you sell or refinance soon. |

| Can improve affordability and cash flow. | Rate shopping can be misleading if loan terms differ. |

| Can make refinancing worthwhile in some cases. | A lower payment can tempt borrowers to overbuy. |

17. Frequently Asked Questions About Mortgage Interest Rates

17.1 What is a good mortgage interest rate?

A good mortgage rate is one that is competitive for your credit profile, loan type, down payment, property, and market conditions. Compare written quotes from multiple lenders rather than relying on averages.

17.2 How do mortgage interest rates work?

Mortgage rates determine how much interest you pay on the remaining loan balance. Each monthly payment covers interest first, then reduces principal.

17.3 What affects my mortgage rate the most?

Major factors include market rates, credit score, down payment, loan type, loan term, debt-to-income ratio, property type, and whether you pay points.

17.4 Does the Federal Reserve set mortgage rates?

No. The Federal Reserve does not directly set mortgage rates. Its policy decisions influence broader credit markets, but mortgage rates also depend on Treasury yields, investor demand, inflation expectations, lender costs, and borrower risk.

17.5 What is the difference between interest rate and APR?

The interest rate measures the cost of borrowing. APR includes the interest rate plus certain loan costs, making it useful for comparing total loan cost.

17.6 Should I choose the lowest mortgage rate?

Not automatically. A very low rate may require expensive points or higher fees. Compare total costs and your expected time in the home.

17.7 Should I pay discount points?

Paying points may make sense if the monthly savings exceed the upfront cost before you sell or refinance. Calculate the break-even period first.

17.8 Can I negotiate a mortgage rate?

Yes, in many cases. You can compare lenders, ask about matching offers, choose different points or credits, and improve your borrower profile before applying.

17.9 How often do mortgage rates change?

Mortgage rates can change daily or even during the day because lenders respond to market conditions and investor pricing.

17.10 What is a mortgage rate lock?

A rate lock is a lender agreement to hold a specific rate for a set period, such as 30, 45, or 60 days, while your loan moves toward closing.

17.11 Is a fixed-rate mortgage better than an ARM?

A fixed rate is better for stability. An ARM may be better for some borrowers who expect to sell or refinance before the adjustable period, but it carries future payment risk.

17.12 Why is my quoted rate different from advertised rates?

Advertised rates often assume specific credit scores, loan amounts, down payments, property types, points, and lock periods. Your actual rate depends on your details.

17.13 Can refinancing lower my mortgage rate?

Yes, refinancing can lower your rate if market rates or your credit profile improve. But closing costs matter, so calculate break-even before refinancing.

17.14 Do shorter mortgage terms have lower rates?

Often, shorter terms such as 15 years may have lower rates than 30-year loans, but the monthly payment is usually higher because repayment is faster.

17.15 How can I get the lowest mortgage rate possible?

Improve credit, reduce debt, save for a stronger down payment, compare lenders, consider the right loan term, and evaluate points carefully.

17.16 Sources Consulted

This article is based on general mortgage education principles and consumer guidance from authoritative sources, including:

- Consumer Financial Protection Bureau (CFPB): mortgage rate comparison, Loan Estimate guidance, fixed-rate vs adjustable-rate mortgage explanations, and discount-point consumer warnings.

- Federal Reserve: consumer mortgage refinancing education and selected interest-rate data used to understand broader rate-market context.

- Fannie Mae: explanations of mortgage-rate construction, the relationship between mortgage rates and Treasury benchmarks, and mortgage glossary concepts.

- USA.gov: overview of CFPB consumer protection role.

- Freddie Mac, HUD, FHA, VA, USDA, and state housing finance agencies may also be relevant depending on the specific loan program.

18. Conclusion: How to Think About Mortgage Interest Rates

Mortgage interest rates are not just numbers on a lender quote. They shape your monthly payment, your long-term cost, your refinancing choices, and your overall housing affordability. The best mortgage decision is not always the loan with the lowest advertised rate. It is the loan that fits your budget, timeline, risk tolerance, and total cost after fees.

Before choosing a mortgage, compare multiple written Loan Estimates, understand the difference between interest rate and APR, calculate the break-even point for points or refinancing, and avoid borrowing more than your household can comfortably support. A smart mortgage rate decision can protect your cash flow today and your financial flexibility for years.

Reader Advice: This article is written for educational purpose only and should not be taken as personalized financial, legal, tax, or mortgage advice. Mortgage rules, lender overlays, interest rates, assistance programs, and eligibility standards can change. Always verify details with licensed mortgage professionals, official program sources, and your lender before making a home-buying decision. Borrowers should compare current lender offers and consult qualified professionals before making a decision.